The Coming Tax Trap: How Nation-States Will Try to Keep You In

They need your taxes. You don't need their territory. Here's what happens next.

Note : This article is the 2nd article in a series exploring how technology, global mobility, and new power dynamics are set to disrupt nation-states, redefine the global economy, and reinvent governance in the 21st century. Here are the first articles in the series:

Many states will see their power diminish as a growing share of their population becomes more mobile and starts behaving like customers, because the power of governments is based on the immobility of their subjects (see the 1st principle in the previous article or in “10 Principles of History for predicting the future”).

Now, when a power structure is disrupted, it does not surrender without a fight, even if the outcome depends on external conditions it cannot control (9th principle).

And when a population tends to move away from them, thereby shrinking their tax base and labor force, many governments are tempted to restore control by tying that population to their territory by various means, including the most extreme ones. Those means always reduce the freedom of their subjects (continuation of the 1st principle).

However, government is limited in its ability to fight disruptions caused by value-creating technologies, because states that win temporarily by banning or stifling a technology lose in the long run, since they do not benefit from its fruits (4th principle).

The issue is that the most economically productive segment of this mobile population will also be the most educated, and it will increasingly use principles of asymmetric defense to take advantage of the 5th principle - a reversal in the balance of power between offensive and defensive technologies is highly disruptive for those in power - which will make it very difficult for states to keep them within their tax systems.

Nation-states face a major challenge: the growing mobility of their most productive population. This trend directly threatens their power, which has historically been based on the immobility of citizens.

The problem is especially acute because:

The richest 10% generate 60-70% of tax revenue (as we saw in a previous article).

This mobile population is generally the most educated and the best able to use technology to evade state control.

Attempts to restrict that mobility may accelerate departures.

To adapt, nation-states will have two broad options:

Try to prevent their population from leaving, at least fiscally,

And attract as many foreigners as possible onto their soil.

Trying to Prevent Their Population from Leaving (At Least Fiscally), and Putting in Place Other Increasingly Desperate Measures to Manage the Economic Situation

“The more I examined [the state’s] efforts at sedentarization, the more I came to see them as a state’s attempt to make a society legible, to arrange the population in ways that simplified the classic state functions of taxation, conscription, and prevention of rebellion”

James C. Scott, Seeing Like a State

We are going to see more and more countries implement :

Exit taxes, in one form or another.

Attempts to tax their expatriates, whether on the basis of nationality or other criteria.

A blacklist of tax havens, or “forbidden” countries, that would automatically trigger taxation in the country of origin for X years after a move, as Portugal and Spain already do for 5 years.

Increasingly heavy taxation of the population that remains in the country.

Measures that could go as far as confiscating part of savings and bank accounts in the event of an economic crisis, as happened in Cyprus.

A reduction in the services states provide, especially the welfare state, in both scale and quality.

Currency debasement through money printing, which will fuel inflation and constitute a second form of taxation for the population.

Regulation of advice that encourages people to leave their country, and, in the most extreme cases, an outright ban.

Cartels with other states in an attempt to reduce tax competition among them (we will come back to this in more detail a bit later).

Generally speaking, the longer you wait before leaving, the harder it will be to free yourself fiscally from your country of origin.

Not that it will become impossible: as we saw in this series, it is difficult for states (except for the United States, with its nationality-based taxation) to fight this effectively. But they will still be able to throw obstacles in your way.

In the long run, states will fail, even if they manage to make all tax exile illegal: one only has to look at the results they get when trying to regulate illegal immigration to understand how hard it will be for them to regulate illegal emigration.

Thus, even the all-powerful United States had an estimated population of about 10.5 million illegal immigrants in 2019; Great Britain, despite being protected by its surrounding seas, has between 594,000 and 745,000 illegal immigrants; and France has between 600,000 and 700,000.

The European Union recorded 330,000 irregular entries in 2022, and the number of undetected entries is of course unknown.

How many illegal tax exiles will manage to get away?

Trying to Attract the Mobile Population of Other Countries

This is a corollary of growing individual mobility: yes, it makes part of your population want to leave, but it also makes part of the population of other countries want to leave.

The growing mass of digital nomads will acquire more and more economic weight, so more and more governments will ask themselves how to attract part of this mobile population to their country rather than to their neighbors.

Spoiler alert: it will not be by taxing them heavily.

More and more countries will therefore put in place:

Light tax systems offered only to people who are not citizens, or who have not been tax residents for years, in order to attract the mobile population of other countries.

Easy-to-access visas for digital nomads.

And, surprisingly, this trend will not necessarily contradict the one we have just analyzed: yes, there will be countries that both 1) heavily tax their own citizens while trying to do everything possible to stop them from leaving, and 2) offer much lighter tax conditions to foreigners, rolling out the red carpet for them.

We saw some examples of this subject in this series. This is because some governments will try, pragmatically and without worrying too much about consistency, to maximize their revenue.

In every case, understand this: your country of origin is never going to roll out the red carpet to make you stay. It takes you for granted. On the contrary, it will throw obstacles in your way to stop you from leaving.

International Cooperation to Try to Tax Multinationals

Such cooperation is already mandatory, because nation-states are already an entity outpaced by current issues: no nation-state, not even the powerful United States, can protect itself against Internet-driven disruption on its own, unless it erects a Chinese-style Great Firewall, which would still amount to following the 4th principle.

In addition, the OECD cartel, still following principle number 9, will not surrender without a fight and will try - in addition to Pillars 1 and 2, which we discussed in a previous article - to put other regulations in place and to lower the thresholds at which they kick in.

States are therefore multiplying their collaborations and will continue to do so in the future, winning battles here and there, but not enough to win the struggle.

Because game theory shows us that the equilibrium of cartels is unstable, and several of their members are always tempted to cheat or use “legal” loopholes to act in their own interest.

It is likely that the 21st century will see the United States cease to be the greatest superpower, or at least cease to be the only superpower. This multipolar world will make international tax cooperation all the more difficult, as we saw during the war between Russia and Ukraine.

Moreover, the multinationals being targeted have immense resources that they do not hesitate to use to optimize their tax burden. American companies, often founded by entrepreneurs with libertarian convictions, seem less reluctant to adopt such practices. However, as democratic nation-states lose credibility by imposing regulations contrary to the fundamental principles discussed in previous articles, a growing number of multinationals will see this as acceptable, even necessary.

Some will even see it as a moral duty.

So we are going to see:

Countries that will display an official 15% corporate tax rate in order to comply with OECD Pillar Two, but that will in practice offer subsidies and other advantages so that the effective rate is far lower.

Multinationals that will find loopholes in the system, including these already obvious ones:

Since the countries in which subsidiaries are located will have the right to tax parent companies if they are not taxed at 15%, some multinationals will shut down subsidiaries in the greediest countries in this regard.

This will be especially true for companies that are primarily present on the web.

Some multinationals will have a headquarters and subsidiaries only in accommodating countries - either non-signatories to the agreement or champions of “paper validation,” displaying an official rate that is in practice much lower.

Again, these will mainly be digital-native companies, but the economy will increasingly be native to the web.

Finally, some multinationals will keep their revenue just below the trigger threshold, either genuinely or artificially, by multiplying entities.

And others will simply withdraw physically from the most troublesome countries.

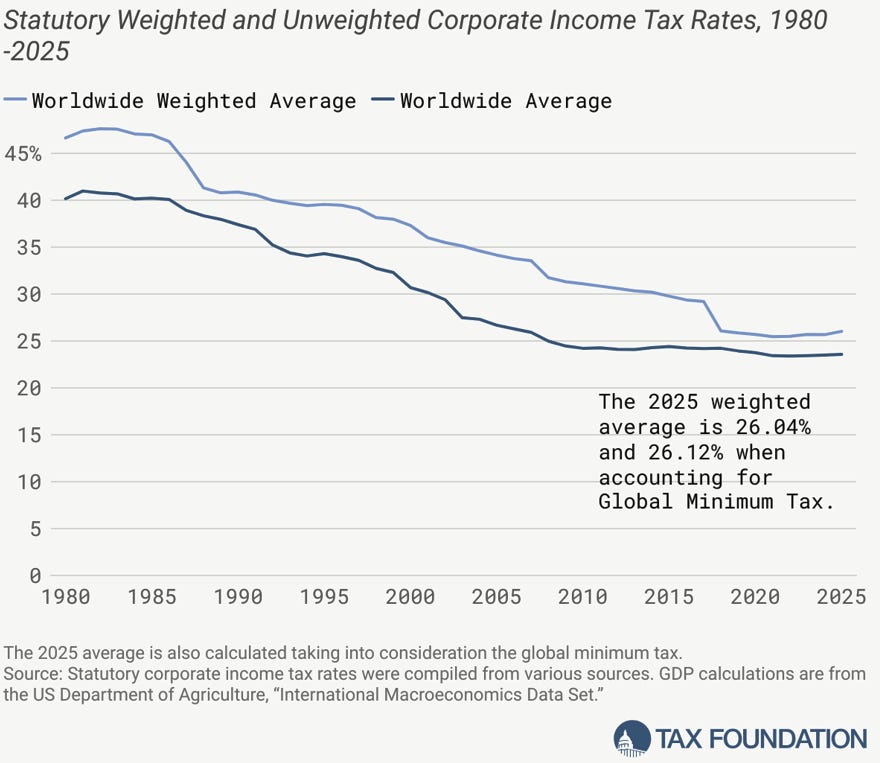

And note that even if the cartel works, a 15% rate is an admission of weakness. In 1980, the weighted average corporate tax rate was 46.52%, and no cartel was needed to impose it1.

Exploding Complexity and Cost

All these “collaborations” to try to align nearly 200 countries with divergent interests and different rules can only happen through bloated bureaucratic systems full of compromises and exceptions, which will explode compliance complexity and costs and create fertile ground for endless appeals and loopholes.

Thus, accounting costs for multinationals rose by 32% from 2017 to 2023, and this complexity also affects SMEs disproportionately.

The Exile of “Ordinary” Businesses

Many web entrepreneurs running small businesses will leave their country of origin in order to take advantage of the market of jurisdictions competing to attract them.

In time, there will be tens of millions of them worldwide.

Some will have offices with employees in their country of exile, but many will have entirely remote teams, generally made up of freelancers, with a mix of people in developed countries, in developing countries, and nomads.

Faced with their growing numbers, nation-states will try to throw obstacles in their way (again, principle 9). They may try various methods.

Creating a Tax on Products Sold from Abroad by a Business with No Physical Presence

Of course, such taxes already exist for many imported goods, but there are few for digital products, aside from VAT here and there around the world, especially in the European Union.

But nothing stops countries from imposing a 100% tax, for example, on digital products sold by companies with no physical presence on their territory.

However, there will be several major obstacles to implementing such taxes.

First, some countries will not be able to impose that tax on countries in the same bloc (such as the European Union or Mercosur, or the states or provinces of federations), but will be able to impose it on countries or states outside the bloc.

However, it will be possible to avoid such a tax by remotely creating a company in a country of the bloc, or in a state of the federation, in order not to be subject to it. Some countries and states will specialize in this niche, as already happens today with Estonia in the European Union and New Mexico in the United States.

Then the major problem, of course, as we have already seen repeatedly throughout in previous articles, is that enforcing a tax or a law on a territory where you are not allowed to send officials with enforcement power is extremely difficult. Again, any company outside the European Union selling digital products is supposed to pay VAT in the customer’s country since 2003, and again, among the hundreds or thousands of American, Canadian, Brazilian, and other entrepreneurs who have sometimes sold tens of millions of dollars’ worth of products, I don’t know of a single one who has ever received the slightest communication on the subject.

And yet VAT is by far the highest-yield tax, and collecting it is the number-one priority of states.

Using the 11th Principle

Helpless in the face of sheer numbers, states will use principle number 11 and attack bottlenecks - payment processors and marketplaces - forcing them to collect these taxes automatically at source.

This will work for multinational companies that follow the rules, such as PayPal, Stripe, or Amazon, that is, enough for the tax to be partly collected.

That is what happened in 2024, when the European Union forced payment processors located within its borders to send information on all intra-EU sales. Sales made in Europe by companies located outside the Union are reported by the financial service used by the buyer, generally the bank or the card issuer.

Eventually, the obligation will probably extend to foreign payment processors that have a physical presence in the European Union through branches.

But there will always be obscure payment processors, located in a single geographic location (often a little-known and uncooperative country), and fraudsters will share information about them on specialized forums.

Some entrepreneurs will even make a business model out of it, offering payment processors knowingly designed to be non-compliant with regulations while outwardly appearing compliant.

If those payment processors are ever attacked by the public authorities of the countries concerned - enough to truly worry them, which will be rare - the entrepreneurs behind them will simply close the targeted company and open a new one, perhaps in another jurisdiction.

In addition, and increasingly, some web entrepreneurs will display a discounted price for customers paying in crypto or through such non-compliant systems compared with the price shown to those paying through compliant payment processors.

The amount of the discount will of course be exactly equivalent to the tax that would have been paid through a compliant system:

EUR1,200 when paying through Stripe.

EUR1,000 when paying in crypto “to encourage the development of cryptocurrencies,” for example.

Just one possibility among others.

This phenomenon will be more common in some countries and cultures than in others, but overall it will be relatively widespread.

Of course, many entrepreneurs will choose not to bother and will pay the tax, if it is reasonable and if payment processors take care of it automatically.

But many others will not play along, and that will create competition that will motivate some otherwise honest entrepreneurs to offer the option anyway.

That will accelerate crypto adoption.

The Internationalization of Tax Fraud

As nation-states become increasingly effective against tax fraud within their borders - notably through automatic exchange of information, the war on cash, and for some the introduction of CBDCs - they will generate a phenomenon many people will not anticipate.

By making life impossible for fraudsters who remain in the country, states will motivate a non-negligible number of them to leave for other countries.

Why?

Many tax fraudsters are of course driven by greed, but why?

Often because they estimate, consciously or not, that the quality/price ratio of their country’s governance services is not that good.

So if you remove their ability to cheat - thereby increasing the cost of services without increasing their quality - many will be inclined to leave if they can. It is a market, with supply and demand.

Among those who leave:

Some will move to tax havens or much lower-tax countries and stop there, complying with the laws of their country of residence and of their country of origin, in which they still sell.

Some will move to those tax havens or lower-tax countries and continue cheating from abroad. Note that I am not writing “cheating abroad” but rather “cheating from abroad”: they will comply with the laws of the country in which they live, but not with all the laws of the countries in which they sell. And the friction created by borders will make prosecutions very costly and difficult (though not impossible) for public authorities, as we saw in the section on flags.

Countries that drove the fraudsters into exile will lose in every case, because what is preferable: a fraudster who does not pay all his taxes but spends most of the surplus in his home country, or a fraudster who can no longer cheat because he feels the noose tightening, and therefore goes into tax exile, pays even less tax (legally or not), and spends most of the surplus in other countries?

The conclusion is inescapable: in practice, for a state, it is better to have the fraudster on its soil than to push him to leave.

The more mobile the population becomes, the more this problem will arise.

However, governments and administrations are so blind to this fact - because they still assume the population is immobile - that this point of view is literally heresy and is hardly ever considered.

The Importance of the Customer-Service Concept in Tax Audits

Administrations are also blind on this point for the same reason: once you account for this new mobility, the quality of the “customer experience” of a tax audit will become increasingly important.

I challenge any tax-administration officials who may read this text: put in place a system to measure the closure of web businesses, and the departure abroad of their managers, in the three years following an audit, and compare those figures with those of non-web businesses.

I’d bet my hand you will be surprised by the number of web entrepreneurs you push into leaving.

I have lost count of the number of French or Belgian entrepreneur friends of mine who left after a tax audit, outraged at having been treated like cash cows, “sheep to be shorn,” rather than as entrepreneurs contributing through their efforts to the country’s economy. Outraged by what they judged to be a disastrous customer experience.

The reality is : the more mobile individuals become, the more freely they will be able to choose their jurisdiction among all those inviting them in, and the more they will behave like customers. Of course price matters (the amount of tax they pay), but what they get in return - quality of life, sunshine, opportunities, and the quality of relations with the administration - matters just as much.

That means that, all else being equal, entrepreneurs will prefer a country in which the tax auditor genuinely respects them over one in which they do not feel respected.

Coming soon

In the next article, we will dive into one of the most decisive turning points for nation-states: their ability to finance themselves, the slow dismantling of the welfare state, the reshaping of inequality, and the deep transformations these forces will trigger across the global economy.

Stay tuned! In the meantime, feel free to follow Disruptive Horizons on X/Twitter, and join the tribe of Intelligent Rebels by subscribing to the newsletter:

And here are the first articles in this series :

“Corporate Tax Rates Around the World, 2025”, Tax Foundation

Something I keep thinking about is, why don’t we just tax companies and corporate equity, rather than individuals?